Financial Services · M. Saunders · Jun 21, 2026

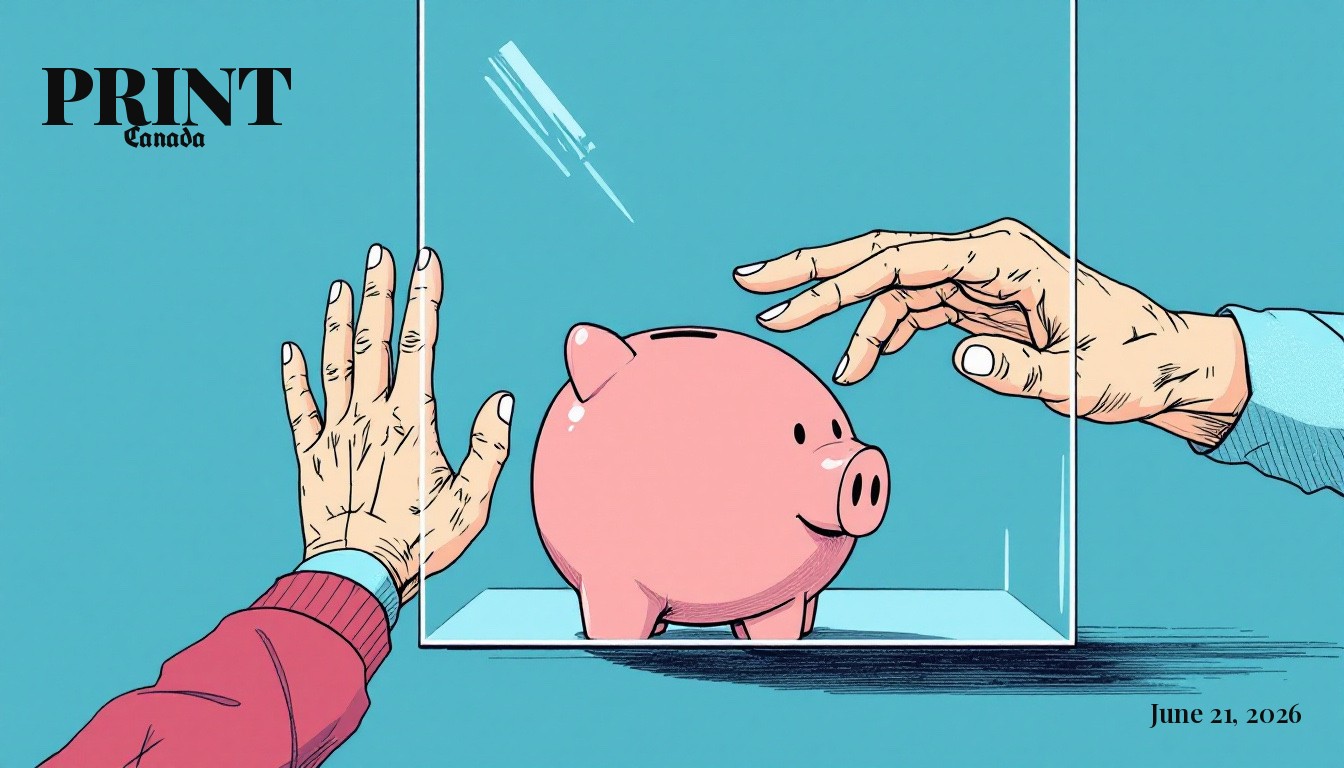

On October 20, 2025, a 72-year-old woman called her insurance company to withdraw $2,500 from her own Registered Retirement Income Fund. She was told it would arrive within a week. It did not arrive. Nine case numbers were opened over the following month. Callbacks were promised and not made. The company cited connection problems, on their end. Three months later, the company sent her a letter admitting it was their fault, offering $5,000, and requiring her to sign away every legal right she had in exchange.